How much to bet?

Why the Kelly criterion works in theory but not in practice

In theory, the Kelly criterion bets most when your edge is highest.

In practice, the Kelly criterion bets most when your mistakes are biggest.

Ask the question — How much should you bet? — of anyone familiar with the topic and it’s 1-to-9 that the response will include the word “Kelly”. According to the classical Kelly criterion, a bettor should bet a fraction of their bankroll equal to edge / odds, assuming edge > 0. This formula is derived by maximizing the expected value of the log-growth rate of a bettor’s bankroll, assuming certain conditions are met (more on this later). Proponents of Kelly insist it is the correct answer to the question of how much to bet. And, indeed, the Kelly criterion has been applied in the development of several profitable betting systems in blackjack, investing, and sports betting.

Yet very few practitioners actually use it.

The closest most bettors come to using the Kelly criterion is by betting fractional Kelly. Under the fractional Kelly criterion, the bettor chooses a fraction 0 < a < 1 and bets a * edge / odds instead.

The predominant argument for fractional Kelly betting is that it reduces variance. This is partially correct, but not for the obvious reasons. On its own, variance is not a bad thing. As gamblers, investors, and risk takers, it’s a fallacy to always seek lower variance. In fact, many gamblers, professionals and recreational alike, enjoy variance. Variance is the underlying asset of gambling, for losers and winners alike. For a bettor who knows he has an edge and has a proven strategy to realize that edge over the long term, extra variance should be treated as an asset, not a liability. (I’ll discuss this point further in a future post.)

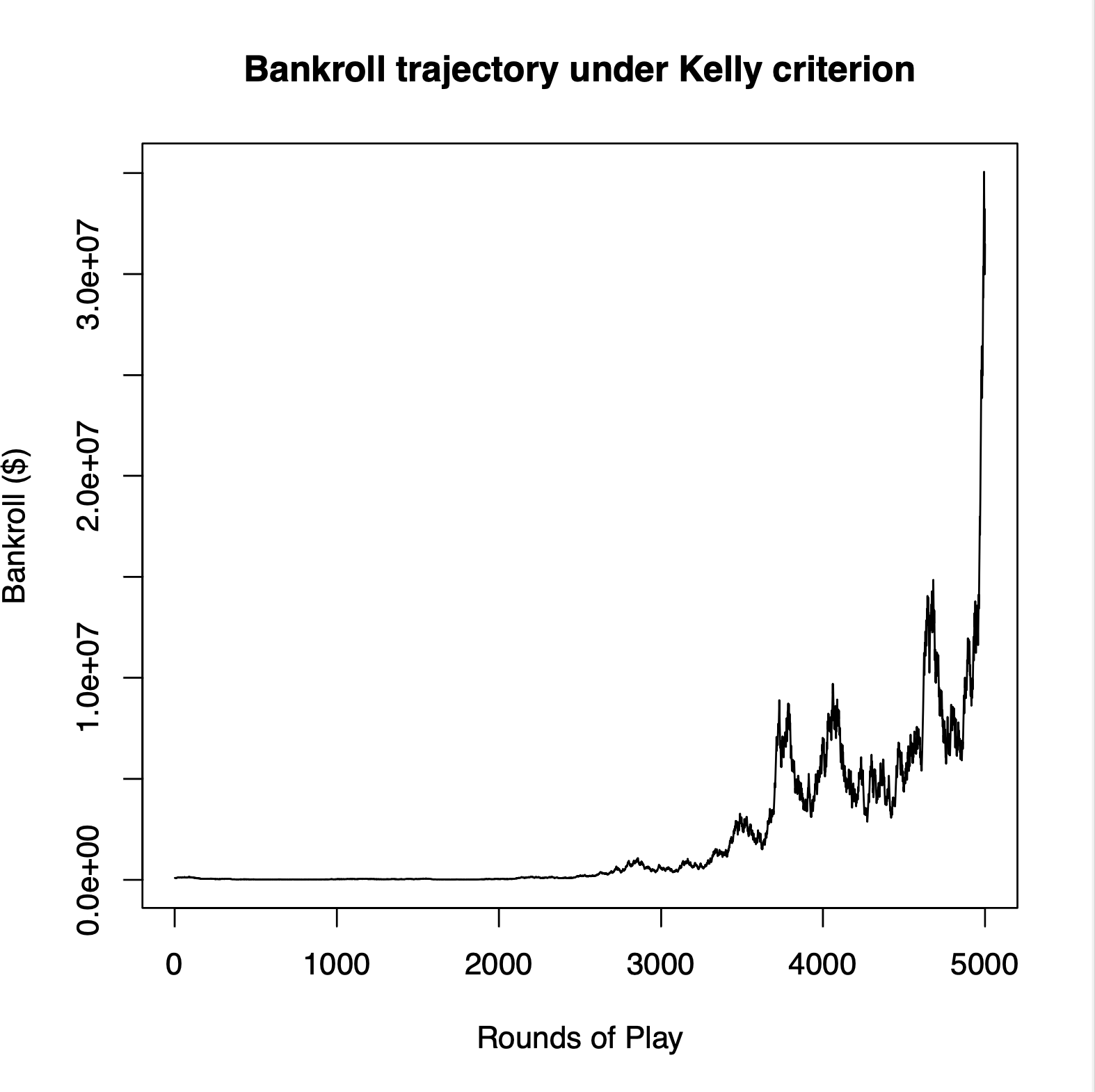

The conventional argument against Kelly will point to a plot like this:

In the above plot, the bettor who started with $100,000 and has a 10% edge has dropped below $20,000 twice and has only half of the original bankroll after 2,000 rounds. In practice, this level of volatility is hard to stomach, but if we knew all the conditions were met and we were applying the Kelly criterion correctly, why would we care about variance? In reality, these conditions are never met, but assuming they were, then we would just close our eyes and keep firing away, knowing that we’re going to eventually reach escape velocity, like this:

So why not close our eyes and fire?

It’s not because we can’t stomach the variance. Actually, variance is critically important to long-term profitability in gambling. Without variance, losers would never win, winners would never lose. The losers would stop gambling — and stop losing. The winners would be too easy to identify — and nobody would gamble with them. The more variance we’re able to handle, the better we’ll be able to sustain an advantage over the long term. But “handling variance” in this case isn’t about emotional control or risk aversion.

The problem with variance is that it prevents us from knowing what we need to know.

In particular, variance prevents us from knowing what our edge actually is — or if we have an edge at all. In the first plot above, how many bettors, after losing 80% of their bankroll almost immediately, would continue betting as if nothing was wrong? At that point, it’s natural to question whether the underlying assumptions are accurate. It may be prudent to quit altogether, but variance prevents us from knowing for sure. The need learn and update on the fly — and to quit before it’s too late — is the primary reason to limit variance (but not too much).

Variance makes losers think they’re winners, and winners think they’re losers

Variance = 1 / Information

The Kelly criterion is optimal only in situations for which we know everything we need to know for the theory to apply. If we knew our edge with certainty and there were no limits (high or low) on how much we could bet, then we could embrace the volatility of Kelly betting and let nature take its course.

In other words, the Kelly criterion is never optimal in practice.

In practice, we never know everything we need to know. At best, we think we know what we need to know, and we cautiously implement it in practice and continually update our opinions as more information comes in. Fractional Kelly betting (half-Kelly or quarter-Kelly) are commonly suggested to mitigate this lack of information and reduce variance. But why is half- or quarter-Kelly a magic number that applies across the board to any situation? Of course, there’s no universal magic number.

The problem with Kelly betting (or half Kelly or quarter Kelly) is that if we wrongly believe we have an edge, it doesn’t matter what fraction of Kelly we use, we’re still going to lose all of our money eventually. In such cases, fractional Kelly only delays the obvious: we go broke more slowly (and with less of a thrill).

How much variance is too much?

The best way I know to answer is: variance is too much if it prevents us from figuring out what we need to figure out before it’s too late. What exactly this means varies depending on what we need to figure out and how much we’re willing to risk in order to find it out.

We bet in order to realize our estimated advantage, and we track results in order to confirm that our estimated advantage is an actual advantage (i.e., that our expected value is actually value expected). To do this systematically it’s beneficial to think about which situation would need to occur in the short term in order for us to rethink our advantage, and to set up a strategy so that if that situation does occur then we actually do have enough evidence to stop betting.

Suppose we start with a bankroll of $100,000. We estimate our edge to be 10% on an even money (1-to-1) bet. Ask the question: What would need to happen for us to question whether our estimated 10% edge is real? For example, suppose we lose more than half of our bankroll within the first 1,000 rounds of play. If this happens, we know that we’ll begin to question our edge and probably abandon the strategy altogether.

But should we? Does losing 50% of our initial bankroll within the first 1,000 rounds provide enough information to conclude we should quit?

To answer this, we compute the probability of experiencing a loss of 50% or more during the first 1,000 rounds of Kelly betting if our edge is correctly estimated at 10%. We find that this probability is approximately 46%. In other words, it’s not very unlikely at all.

For comparison, the probability of a 50% drawdown (or more) if we bet full Kelly assuming an edge of 10% when we in fact have no edge is 98%.

The point of computing these probabilities is not to calculate the probability that we do or don’t have an edge — that is not what these probabilities mean — but rather to devise a strategy that allows us to learn about our true edge at a rate we’re comfortable, and to be decisive about quitting once we’ve gained sufficient evidence.

The ratio of the above two probabilities is called the likelihood ratio (LR) and can be used as a measure of how much evidence the specific event offers that our initial belief is wrong. In this case, LR = 2.1 means that we’re only about twice as likely to lose 50% or more if we have no edge as when we actually have the 10% edge we assumed. If you ask me, that’s nowhere near enough evidence to determine one way or another.

Variance is too much if we are very likely to end up in an uncomfortable situation and not know whether we should quit or keep going.

We don’t want to put ourselves in an uncomfortable situation — losing half of our money — and not knowing whether we should quit (and potentially give up on a profitable opportunity) or keep going (and potentially lose more money chasing a losing opportunity).

To avoid this situation we can either adjust our stop loss — for example, instead of considering a 50% drawdown, consider an 80% drawdown — or modify our strategy in order to reduce the probability of the 50% drawdown.

Here are some possibilities:

Full Kelly: Prob of losing 80% or more in the first 1,000 rounds: 19% (LR = 5.4)

Full Kelly: Prob of losing 90% or more in the first 1,000 rounds: 9% (LR = 10.5)

Notice a few things. First, though it’s not likely that we’ll experience a downturn of 80% or 90%, it’s also not very unlikely. Such outcomes are far from remote or unusual. So even though such an occurrence offers some evidence that we don’t have the edge we originally believed, it’s not really enough to definitively conclude that we should quit. Second, to add insult to injury, even if it were enough evidence to conclude we should quit, the lesson would have cost us almost our entire bankroll. As a rule of thumb, we should try to avoid situations where we lose almost all our money and still don’t know what happened — did we make a mistake or just get unlucky?

In practice, we want an approach that allows us to make more definitive conclusions more quickly.

And that’s the main reason for the Kelly criterion is too aggressive. It doesn’t allow us to learn fast enough to prevent disaster. The less we know, and the more we need to learn about our edge, and the more variance works against us.

With this in mind, let’s consider the same questions, but assuming we bet a fraction of Kelly instead of 100% Kelly. Here are the probabilities and likelihood ratios of losing 50% during the first 1,000 rounds under different fractional Kelly strategies:

100%-Kelly: 46% (LR = 2.1)

50%-Kelly: 11% (LR = 7.4)

25%-Kelly: 0.8% (LR = 75)

10%-Kelly: <0.1% (LR > 100)

These are empirical values computed by simulating the probability in the specific case described (10% edge at 1-to-1). Similar probabilities can be computed with different parameters and different criteria.

Which Kelly fraction to choose?

The above numbers give some empirical justification for why 25% Kelly seems to be a sweet spot in a lot of practical betting situations. In the example above, 25% Kelly reduces the variance sufficiently so that if we lose a lot of money (defined as 50% of our bankroll in this case), we can be pretty sure (LR = 75) that we’re not just getting unlucky. Half-Kelly, on the other hand, doesn’t offer very strong evidence to definitively conclude one way or the other.

But just because 25% Kelly is a good choice in this situation doesn’t mean it is a universally good choice in all cases. In the example above, both the edge and the probability of winning are moderate, and we arbitrarily chose 50% as the drawdown criterion because it offers a reasonable middle ground between overreacting (quitting too soon) and waiting too long (going broke).

Moreover, we may want to be more or less aggressive depending on our level of confidence about our perceived edge in different situations. As a rule of thumb, instead of arbitrarily using 25% or 50% of Kelly regardless of situation — in reality, the reason everyone picks these values is just because someone else told them, not because of any conscious decision for why these are good choices in a specific situation — we can instead set explicit values for the two key parameters that are within our control: the amount of evidence we need to make a definitive conclusion and the amount of money we’re willing to lose before drawing that conclusion.

Stop criterion: Set the minimum LR value needed in order to conclude there’s no edge and it’s time to quit.

Stop loss: Set a maximum exposure threshold (E), which is the largest amount (either in absolute terms or as a percentage of bankroll) that you are willing to lose on a given strategy.

These criteria can be applied to derive an appropriate bet sizing strategy under various conditions. In situations where we can bet a fraction of bankroll, as discussed below, the suggested approach gives the fractional Kelly percentage that best fits the chosen conditions. In other situations, where we bet a fixed amount and are constrained between fixed minimum and maximum sizes, we can perform the same analysis, with reference to absolute bet amounts instead of fractions of bankroll. Either situation could be best in a given context, but I only discuss the fractional Kelly case below.

The LR criterion simply reflects how much evidence we need to see before we conclude that our initial assessment is wrong. The higher the LR threshold, the less prone we are to overreacting, but the more conservative we have to be in order to stay under our exposure limit. Lower thresholds cause us to overreact more, but also allow us to be more aggressive. The exposure threshold represents how much of our bankroll we’re willing to lose before we reassess the situation.

The exposure limit reflects the intuition that we don’t want to commit our entire bankroll to any given situation, no matter how favorable. Under the Kelly criterion, it is assumed that a bettor will use the entire bankroll (if necessary). But in practice it’s common to set aside an amount that one is willing to risk, either a fixed amount (say, $1,000, $10,000 or $100,000) or as a fraction of total bankroll (5%, 10%, or 25%). This amount is the exposure limit (E).

For a given choice of LR and E, the idea is to bet in such a way that if the exposure threshold is reached or exceeded (lose more than E) then we have enough evidence (above LR) to stop betting.

Now, for the tie in to the Kelly criterion. Recall that the Kelly criterion maximizes the expected value of the log-growth rate of the bankroll, but ignores other factors, such as limited information about our edge and other practical matters. Now that we’ve identified a stopping rule as a way to avoid disastrous situations that matter in practice but aren’t accounted for by Kelly, we can go back to using the Kelly criterion to find the optimal fraction we should bet subject to the additional constraints imposed by our stop criterion (LR) and stop loss (E).

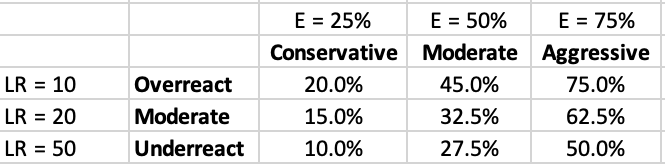

Below are some examples. We set 3 levels of LR threshold (10, 20, 50) to represent levels that are prone to overreacting, moderate, and underreacting. And we set E values of 25%, 50%, and 75% for conservative, moderate, and aggressive. (In practice, these E values are all pretty aggressive, but are chosen here to best illustrate how the bet sizes vary across the range of possible choices.)

Optimal fractions can be computed in any other situation as well. Notice that there is nothing special about any particular Kelly fraction (10%, 25%, 50%, or otherwise). The best choice of Kelly fraction depends on personal bankroll considerations and attitude toward aggression — not an attitude toward volatility or risk.

More aggressive approaches are willing to risk more money, and therefore willing to bet a larger percentage of bankroll than more conservative approaches. The tradeoff is natural: more aggressive bettors will gain more when they’re right, but lose more when they’re wrong. Similarly, decision rules that overreact have more leeway to be aggressive, but at the expense of quitting too soon when a situation is actually favorable.

Very original and practical treatment of Kelly! You make a good argument of the practical limitations of Kelly when there's uncertainty about the magnitude of the edge.

Could Kelly still be useful though for relative sizing of betting opportunities? For example, what if we had an additional even odds bet with a 60% chance of winning, ie a 20% edge should we bet twice the fraction of the payroll than the original 10% edge bet assuming the two bets are independent? What if we had a collection of n independent bets?

What a great article, thanks!